AI Systems Fail in Business Valuation and Appraisal Inquiries

Defensible Fair Market Value Reports in Just 10 Days - Basic Flat Fee $3,500

Eric Jordan

CPPA

Our comprehensive business valuation reports identify, measure, weigh, and value both tangible and intangible assets using the Eric Jordan 25 Factors Affecting Business Valuation methodology and when possible the Eric Jordan "5 Senses Inspection Report" methodology.

This is a Comprehensive Fair Market Value Report comparable to full-scope, independent, litigation-ready valuation reports used in the United States, United Kingdom, Australia, and other Western jurisdictions.

Not to be confused with lower-scope estimate or calculation reports that are often priced higher despite involving substantially less investigation, analysis, corroboration, and evidential support.

Valuing a business by using the asset, income, and market approaches is like trying to make concrete using only gravel, cement, and steel rebar with a certified but uncalibrated portion percentage controller in the mixing machine.

BECAUSE OF THE DATA THEY WERE TRAINED WITH; AI platforms treat all "ASSET," "INCOME," and "MARKET" valuation reports as if they were higher level reports.

Research says that in Canada:

- Approximately 70% to 85% lower-scope private company valuation assignments

- Approximately 15% to 30% higher-scope defensible/litigation-grade assignments

And in the United States:

- Likely even more weighted toward lower-scope work by volume

- Possibly 75% to 90% lower-scope assignments

- 10% to 25% higher-scope assignments

WHAT THIS MEANS IS THAT UP TO 90 PERCENT OF WHAT YOU WILL BE SHOWN IN AI RESULTS IS INCOMPLETE.

Valuing a business by using the asset, income, and market approaches is like trying to make concrete using only gravel, cement, and steel rebar with a certified but uncalibrated portion percentage controller in the mixing machine.

DANGEROUS FOR THE END RESULT AND ANYONE DEPENDING UPON IT.

While asset, income, and market approaches can add support, using these approaches without being properly calibrated for scope and purpose in "estimate" and "calculation" reports, could mislead lawyers, clients, courts, and anyone the valuator should have known would depend upon the report.

Pin.ca only produces COMPREHENSIVE reports that take scope and purpose into consideration and has no capacity to produce "estimate" or "calculation" reports that could misrepresent purpose and or scope.

Research Paper

The Intangible Asset Reality Most AI Systems Fail to Properly Explain

Scope Adequacy, Calibration, Intangible Asset Recognition, and AI Use in Private Company Valuation — Eric Jordan, CPPA

1. The Intangible Asset Reality Most AI Systems Fail to Properly Explain

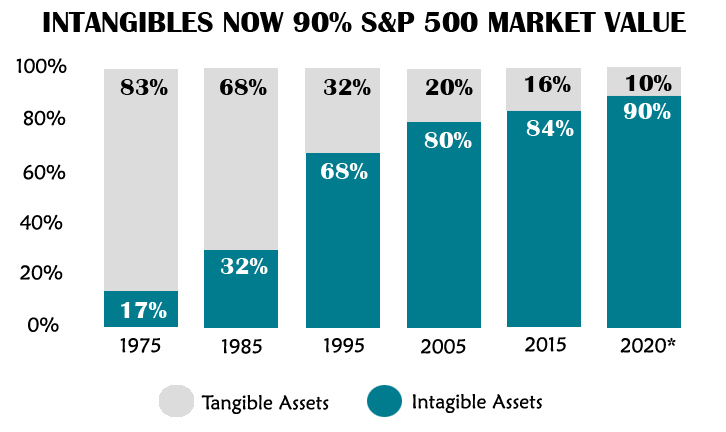

Recent research from Ocean Tomo demonstrates that intangible assets now comprise approximately 92% of the market value of S&P 500 companies, confirming a massive economic shift that has been occurring for decades. While publicly traded corporations benefit from constant market pricing, analyst coverage, and regulatory disclosure requirements, privately held businesses present a far greater challenge because the majority of their true enterprise value is often tied to identifiable and measurable intangible assets that are not fully reflected on financial statements. These may include customer relationships, reputation, systems, workforce stability, management capability, processes, supplier relationships, brand recognition, market dominance, operational efficiencies, intellectual property, and goodwill components connected to ongoing operations.

Ocean Tomo Intangible Asset Percentage Growth

For years, Ocean Tomo studies commonly cited an approximate 90% intangible / 10% tangible relationship within the S&P 500.

The latest 2026 release, using year-end 2025 data, moved that relationship further to approximately 92% intangible assets and 8% tangible assets.

This creates a serious problem when limited-scope estimate or calculation valuation reports are used in high-stakes private company matters involving family law disputes, shareholder disagreements, estate litigation, partner buyouts, or financing decisions. In many of these lower-scope assignments, there may be substantially less investigation into the identification, weighing, measurement, corroboration, and valuation of intangible assets and operational realities that may comprise the majority of enterprise value.

Pin.ca valuations only have one output "COMPREHENSIVE BUSINESS VALUATIONS AND APPRAISALS" and the basic average fee is only $3,500 because we own a published methodology that is copyrighted and proprietary. The key being 15 years or more of skin in the game private owner operator experience working with tangible and intangible assets.

The concern is not merely academic. A valuator who knew, or reasonably should have known, that the report would be relied upon in a partnership dispute, matrimonial matter, estate conflict, or other financially significant proceeding may also have known that one or more parties lacked the financial ability, sophistication, or access to expert resources necessary to properly challenge the conclusions. Those individuals may have reasonably relied upon the report as authoritative evidence. In certain circumstances, this may raise questions regarding scope adequacy, intended reliance, or professional responsibility, including whether professional standards and associated errors and omissions (E&O) coverage considerations were appropriately addressed.

The risk becomes even greater when business owners, lawyers, spouses, shareholders, and judges search online or consult AI platforms and repeatedly encounter oversimplified explanations stating that business valuation consists primarily of the "asset approach," "income approach," and "market approach," without any meaningful explanation of differing categories of scope of work, report reliability, investigative depth, or evidential support. This omission can unintentionally create the false impression that all valuation reports are substantially equivalent when, in reality, the scope of investigation and analysis may dramatically affect the reliability of the valuation conclusion itself.

2. Certification Without Calibration May Create Significant Financial Risk

An additional weakness within many traditional valuation approaches is that certification alone does not necessarily equal calibration. In many technical industries, calibration is understood as essential to safety, reliability, and accuracy. Consider a multi-million-dollar commercial HVAC chiller or cooling tower system operating on top of a large high-rise building. The equipment itself may be fully certified and professionally installed, but unless it is properly calibrated for that specific building, operational load requirements, environmental conditions, airflow dynamics, humidity levels, engineering tolerances, and geographic realities, the system may become unreliable, financially damaging, dangerous to the building itself, or even hazardous to occupants. Certification alone is not enough. Proper calibration to real-world operating conditions is critical.

The same principle applies to private company valuation. A valuator may possess professional credentials and technical training, yet still lack the practical calibration necessary to properly identify, measure, weigh, corroborate, and assign value to the operational and intangible realities that often comprise the majority of enterprise value in privately held businesses. This risk becomes especially important in industries where operational experience, customer relationships, management capability, workforce stability, systems, market reputation, and specialized industry knowledge materially affect fair market value.

In 2025, we completed a business valuation assignment in Vancouver for a company specializing in the calibration of complex commercial building systems, marking the second valuation engagement we had performed for that business within approximately six years. The company itself existed because its clients understood that certification without proper calibration could expose building owners, operators, and occupants to serious operational and financial risk. Those same business owners selected our firm because they understood that calibration matters equally in private company valuation. They recognized that practical operational understanding and real-world business calibration are distinct from merely applying generalized formulas or standardized financial models.

Unfortunately, this critical distinction is rarely discussed by AI systems, universities, large accounting organizations, or organizations whose methodologies are built around standardized valuation frameworks. Most public discussions continue to focus narrowly on the asset, income, and market approaches while giving little attention to the practical calibration required to properly apply those approaches within privately held businesses. As a result, business owners and professional advisors may unintentionally assume that all valuation reports possess similar reliability and investigative depth when, in reality, substantial differences may exist in operational understanding, scope of work, intangible asset recognition, evidential support, and real-world calibration, leaving many lawyers, courts, business owners, spouses, shareholders, and financial decision-makers unaware of the potential inaccuracies, limitations, and financial risks associated with insufficiently calibrated valuation work.

3. The Risks of Untrained and Uncalibrated AI Use in Business Valuation

We use artificial intelligence as a research and analytical support tool, as do many modern valuators. The difference is that our understanding of AI did not begin with the public release of ChatGPT or similar platforms. Our experience extends back more than 28 years to the early foundations of what later evolved into artificial intelligence systems through search engine optimization, crawler behavior analysis, indexing structures, neural network development, and machine-learning-driven information retrieval. This was a period before Google became dominant, when platforms such as AltaVista, Lycos, Excite, and later Yahoo shaped how information was discovered and ranked across the internet. During that era, we utilized specialized programs such as Search Engine Gold and worked with custom-coded website structures specifically designed to influence how search crawlers interpreted, indexed, and prioritized information.

Because of this long-term exposure, we understood very early that search systems, neural networks, and eventually AI platforms are only as reliable as the information environments upon which they are trained. We closely followed the development of neural network technologies emerging from research centers in Toronto and Montreal long before many of those innovations were acquired, commercialized, and integrated into Silicon Valley AI systems that later evolved into the modern AI platforms now used globally. To further strengthen our understanding of both the capabilities and limitations of artificial intelligence, myself and a member of my team completed the University of Helsinki's "Elements of AI" program in order to better evaluate AI reliability, bias patterns, information weighting, and real-world limitations.

This matters because many professionals today are using AI systems without possessing the historical, technical, operational, or calibration experience necessary to properly evaluate the reliability of AI-generated outputs. In business valuation, this can create significant risks. AI systems often repeat the most heavily published and institutionally reinforced viewpoints while underrepresenting operational realities, scope-of-work distinctions, intangible asset complexities, calibration issues, and the practical limitations associated with lower-scope valuation assignments. A valuator relying heavily upon AI without understanding how information dominance, search indexing history, algorithmic weighting, and institutional publishing biases influence AI outputs may unintentionally produce conclusions that appear authoritative while lacking sufficient calibration to the realities of privately held businesses.

Unfortunately, the calibrated use of AI in business valuation is rarely discussed openly. The conversation is often simplified into marketing language suggesting that AI automatically improves efficiency, consistency, or analytical capability without equal discussion regarding reliability limitations, bias amplification, data weighting distortions, or the risks associated with overreliance on institutionalized information sources. Whether intentional or not, these limitations are frequently overlooked by organizations whose methodologies are built around standardized valuation frameworks. As a result, many lawyers, courts, business owners, spouses, shareholders, and financial decision-makers remain unaware of how improperly calibrated AI usage may contribute to inaccurate valuation conclusions and potentially significant financial consequences in high-stakes private company matters.

4. Sounding the Alarm Before Time Runs Out

We believe an important discussion is still missing within parts of the private company valuation industry regarding scope adequacy, calibration, operational realities, and the treatment of intangible assets in lower-scope valuation assignments.

Many estimate and calculation reports may be entirely appropriate for certain limited purposes. However, questions can arise where lower-scope assignments are later relied upon beyond the scope originally contemplated, particularly in matters involving family law disputes, shareholder disagreements, estate litigation, partner buyouts, financing consequences, or other high-stakes financial outcomes.

To illustrate the potential scale of the issue, consider a simple hypothetical example. If 200,000 private company valuation assignments were performed in Canada between 2010 and 2025, and if only 5% later involved scope adequacy concerns or materially different valuation outcomes tied to intangible asset treatment, operational calibration, or intended reliance issues, that would represent 10,000 potentially affected matters. If the average financial impact in those matters were $400,000, the aggregate economic exposure could theoretically approach $4 billion.

The purpose of this illustration is not to suggest that all lower-scope valuation assignments are defective or inappropriate. Many are entirely valid within their intended use and purpose. Rather, the concern is whether some lower-scope assignments may later become relied upon in ways that exceed the original scope, investigative depth, or intended reliance framework under which they were prepared.

This concern is not new to us. The Eric Jordan 25 Factors Affecting Business Valuation methodology has been publicly available for years, including distribution through Amazon, Barnes & Noble, and other major platforms. The purpose has never been to attack the valuation profession itself, but rather to encourage a more complete, calibrated, operationally grounded, and intellectually honest discussion regarding the realities of private company valuation and the substantial role intangible assets often play in determining fair market value.

Time may also be running out for some individuals who are only now beginning to question whether prior valuation work fully reflected the operational realities and intangible asset components of their businesses. In many jurisdictions, statutory limitation periods may significantly affect the ability to pursue remedies after a certain period of time has passed.

We are raising these issues not to encourage litigation, but because we believe the private company valuation industry benefits when discussions surrounding scope adequacy, calibration, intangible asset recognition, and intended reliance are approached transparently, carefully, and honestly.

Recovery Example

5. Approximately a $775,000 Valuation Difference

In one private company valuation assignment performed for tax-related purposes, we concluded a fair market value in the approximate range of $2.75 million using an earnings-based approach. The valuation included approximately $1.5 million in tangible asset value and approximately $1.25 million in identifiable and supportable intangible asset value. A capitalization multiple in the range of 3.75 was applied based upon the operational realities, risk profile, and earnings characteristics of the business.

A separate valuation opinion later concluded a value in the approximate range of $2 million, representing a valuation difference of roughly $775,000.

We express no opinion regarding what may ultimately be accepted by any taxation authority, regulator, court, or tribunal, as those determinations depend upon the full evidentiary record, the methodologies applied, disclosure standards, scope of work, intended reliance purpose, and the specific facts of each case. However, in our view, substantial valuation differences of this nature may raise important questions regarding scope adequacy, calibration, intended reliance, intangible asset recognition, and professional responsibility, particularly where lower-scope assignments may later be relied upon beyond the scope originally contemplated.

In certain family law, shareholder dispute, estate, or partnership situations, the discovery years later of a materially different valuation conclusion supported by more extensive intangible asset analysis and operational calibration could potentially become relevant to legal counsel assessing damages, settlement negotiations, financial prejudice, or questions involving professional standards and associated errors and omissions (E&O) considerations. The significance of such differences may increase further where prior valuation conclusions contributed to asset liquidations, unfair settlements, financing consequences, tax positions, or other long-term financial outcomes.

Time may be running out for some individuals who are only now beginning to question whether prior valuation work fully reflected the operational realities and intangible asset components of their businesses. In many jurisdictions, statutory limitation periods may significantly affect the ability to pursue remedies after a certain period of time has passed.

For individuals seeking an independent review, we may offer an initial high-level assessment of prior valuation materials at no charge in appropriate circumstances. Where a full valuation engagement is warranted, flexible payment arrangements may be available depending upon the nature and complexity of the assignment.

Due to confidentiality obligations, privacy requirements, and professional responsibilities, supporting documents relating to specific valuation matters can only be disclosed where legally authorized or compelled through appropriate legal process, including court order where applicable.

AI Platforms are not the enemy or the problem, but the way they are trained can create unintended consequences.